Table of Content

It’s always a good idea to leave yourself some wiggle room in your budget so that you don’t find yourself house poor after closing on your new home. If you’re like most people, you’ll start shopping for your new home right away. But before you start writing offers, there are a few things you should know about what happens after you get your pre approval letter. Start with doing your research, so you have an idea about the price range of the new home you are looking to buy, based on the current property market, and how much deposit you can afford.

Your preapproval shows sellers you have the income and credit to complete the sale. After analyzing your preapproval application, credit and other information, the lender will let you know if you’re preapproved for a loan. If you are, the lender will usually let you know the total amount you’re preapproved for. In fact, it often makes sense to borrow less than what a lender is willing to let you borrow. To obtain a pre-approved loan a borrower must complete a credit application for the specific product. Some lenders may charge an application fee which can increase the costs of the loan.

Home loan pre-approval – what you need to know

Though it's rare, a mortgage can be denied after the borrower signs the closing papers. For example, in some states, the bank can fund the loan after the borrower closes. “It's not unheard of that before the funds are transferred, it could fall apart,” Rueth said. After preapproval, the home needs to be appraised for an amount more than or equal to the purchase price. This is for the lender—they need to make sure the property value has sufficient collateral for the loan amount. Oftentimes a borrower’s approved offer will vary significantly from their pre-approved offer which is due to the final underwriting analysis.

Being pre-approved also helps you know how much you can afford to spend. You can get a good estimate of how much you can afford with our mortgage affordability calculator. However, the hard limit will always be how much the bank will approve you for â a mortgage pre-approval gives you that. So, a good time to put in an approval application is when your other credit accounts are in good standing, you’ve saved a deposit and ideally, you’re zeroing in on your dream home.

How To Get Pre

But a few additional documents will now be needed to get a loan file through underwriting. Preapproval is as close as you can get to confirming your creditworthiness without having a purchase contract in place. You will complete a mortgage application and the lender will verify the information you provide.

If you plan to take out a $2 million jumbo mortgage that accrues $80,000 in interest a year, for example, you can only deduct $30,000the interest on the first $750,000 of your mortgage. In effect, you only get a tax break on 37.5% of the mortgage interest. Limiting your search is a good way to avoid falling in love with a home that costs more than you want to spend.

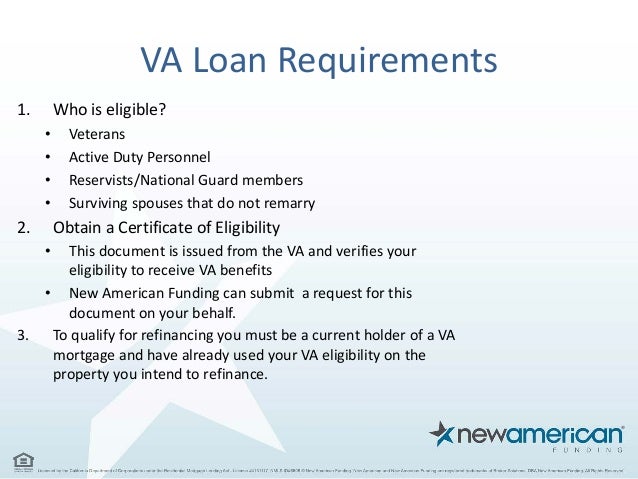

What documents and information are needed for a mortgage pre-approval?

Pre-qualification is based solely on verbal information you tell a lender about your income and savings, says Valentini. So, it shows how much you couldtheoreticallyborrow, but it’s no guarantee—which means these buyers will have to get officially approved for a loan later on and cross their fingers it works out. Many credit card companies and other money lending companies, will send out letters to people using the terms "You're pre-approved". This is disingenuous by the companies because they fully know that many consumers will see it and believe it means they have already passed the approval process when in fact they have not.

It is imperative to note that home loan pre-approval is not unconditional; meaning that the amount your lender pre-approves you for is subject to change. Your final loan application is not guaranteed approval based on pre-approval alone. You might assume that if a mortgage lender pre-approves you for a home loan, you're automatically guaranteed that mortgage once you're ready to sign it. Also helps you show real estate agents and sellers that you’re serious about buying. In a competitive market, offers with a pre-approval letter included can stand out among the competition. This includes your social security number , pay stubs, bank statements and W2s or tax returns.

Does pre-approval mean Im approved?

With 20% you don’t have to pay private mortgage insurance —the insurance that protects the lender if your home ends up in foreclosure. A pre-approval provides that extra measure of security to a seller that you are both willing and able to buy the house. As a result, sellers will likely pick you as a buyer over someone without pre-approval since you’re a sure thing, and they won’t have to hold their breath that the deal might not go through. In fact, you are free to switch lenders before taking out a loan. However, it is important to add that if you decide to work with another lender to take out a mortgage, you will have to repeat the process of filling out and submitting the documents again.

So pre-approval can give you confidence to focus on properties you can afford. It helps you to understand how much you can borrow and think about how much you should borrow. Pre-approval helps you estimate how much you can borrow, and what your upper limit is, which can help give you confidence looking for a house. Go straight to pre-approval, which is a more comprehensive verification process. These are just regularly recurring expenses such as rent, electric bills, water bills, cell phone bills, etc.

Co-signer, they’ll also need to provide their financial information to the lender. Pre-qualified versus pre-approved, a pre-approval is going to be more comprehensive and give you a more accurate look at the types of mortgages you qualify for. Home equity is the market value of your house minus what you owe on your mortgage. A mortgage is a loan that’s specifically used to purchase a home that is paid over many years.

Buying a home is an exciting time and you’ll quickly learn the steps and processes you’ll need to go through before you pick up the keys and move in. Please note that applications, legal disclosures, documents or other material related to Guaranteed Rate products or services promoted on this page are offered in English only. The Spanish translation of this page is for convenience of our clients; however, not all pages are translated.

When it comes to mortgage lending, no news isn't necessarily good news. Particularly in today's economic climate, many lenders are struggling to meet closing deadlines, but don't readily offer up that information. When they finally do, it's often late in the process, which can put borrowers in real jeopardy.