Table of Content

Pre-approval is therefore useful when you have less time and a shorter transaction window for the process. You don’t need to be pre-qualified to start looking at houses, but many real estate agents like to see at least a pre-qualification letter before committing a lot of time and effort to showing you homes. A mortgage pre-approval is not the same as a pre-qualification, but they serve many similar purposes. Both help you estimate the loan amount you’re likely to qualify for.

Most Canadians think the first step in the home-buying process is to contact a realtor and start looking at homes. The first thing you should do is apply for a mortgage pre-approval. After all, if you find a home you like, youâll want to move quickly. Being pre-approved for a mortgage removes an extra step in the process.

Want To Learn More About Buying A Home

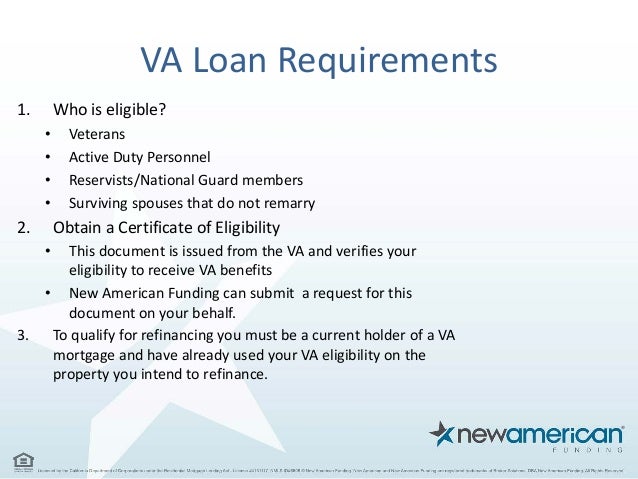

Any regulatory changes in Australia may also affect your loan’s status. And, if your Loan-to-Value Ratio is higher than 80 per cent, you may require Lenders Mortgage Insurance.

Your financial situation is unique and the products and services we review may not be right for your circumstances. We do not offer financial advice, advisory or brokerage services, nor do we recommend or advise individuals or to buy or sell particular stocks or securities. Performance information may have changed since the time of publication. If your loan application is denied post pre-approval it may be best to withhold from immediately placing another application. Each time you apply for pre-approval, or a loan, this will be marked on your credit report as an enquiry.

BMO Harris personal loan review: Small loans and broad...

Neither FHA.com nor its advertisers charge a fee or require anything other than a submission of qualifying information for comparison shopping ads. We encourage users to contact their lawyers, credit counselors, lenders, and housing counselors. This is where your lender will check your credit and confirm your financial information. Once approved, your lender is committing a mortgage to you at a set interest rate for a fixed period of time.

However, if you have a significant history of debt, foreclosures or a low credit score, the pre-approval process can take longer, from a few days to as long as several months for some individuals. Providing the lender with all the documents needed can help speed up the process, even with some issues in your credit history. Underwriting for a mortgage loan typically requires a borrower’s credit score and two qualifying ratios, debt-to-income, and a housing expense ratio.

Knowing your buying power

The most obvious Red Flag that you are taking a personal loan from the wrong lender is the High Interest Rate. The rate of interest is the major deciding factor when choosing the lender because personal loans have the highest interest rates compared to other types of loans. Federal law requires a three-day minimum between loan approval and closing on your new mortgage.

Also, changes in your credit reports that occurred after your profile was prescreened may disqualify you. Say a lender reviewed your credit profile when you weren’t carrying a balance on any of your credit cards. If you end up having a financial emergency and have to max out your credit cards to pay for it, your credit reports can substantially change — that difference in your credit reports could result in a denial. Companies review information in your credit reports, or from other third parties, against a set of criteria. If you meet the company’s requirements, then it may send you a preapproved loan offer inviting you to apply for a loan. Getting preapproved for a loan helps sellers feel confident that they aren’t wasting their time with an insincere buyer looking at dream cars or homes they can’t afford.

If you’re applying with a co-applicant, they’ll need to provide the same information. Since completing a pre-approval application does affect your credit score, getting a free check that won’t impact your credit will give you a rough idea of your current score. You can then use the estimate as a baseline for checking if you meet a lender’s mortgage qualifications. While the borrowing options might be narrow, some lenders might offer a mortgage with some added requirements. One of the first details your lender will review is your credit score.

There aren't any great drawbacks to obtaining a single pre-approval, but having several in a short period can potentially harm your ability to borrow. To apply for pre-approval, make an appointment with a Suncorp Bank Mobile Lender online. A handy selection of articles, calculators and services to help you on your property buying journey. The company name, Guaranteed Rate, should not suggest to a consumer that Guaranteed Rate provides an interest rate guaranteed prior to an interest lock. Pre-approval allows prospective buyers to search for a home with an accurate estimate that they can afford. This reassurance not only helps home buyers shop with confidence, but will also go a long way in avoiding potential interruptions to the sale down the line.

A mortgage pre-approval, on the other hand, is a thorough inquiry into your finances. A lender won’t simply ask how much income you make—you’ll have to prove it. Your lender will also pull your credit history, verify your income and assets, and assess your financial situation before they give you a mortgage pre-approval. Getting pre-approved for a mortgage before you make an offer on a house is a smart idea.

Learn more about the pre-approval process below or show sellers and agents that you’re ready to buy now with PowerBid from Guaranteed Rate. While both pre-qualification and pre-approval from a lender help identify your price range, a pre-approval letter can signal to your real estate agent and sellers that you’re serious about buying a home. Agents often require a pre-approval letter, because it is a strong indication that you are a qualified buyer and can make a competitive offer. However, lots of debt, a history of previous foreclosures, and a low credit score can slow down the process.

There are several benefits to obtaining home loan pre-approval, the most significant of these is that you will receive your approximate borrowing capacity figure. Borrowing capacity is calculated on your debt-to-income ratio and outlines the amount that you can borrow. Knowing approximately what you might receive then enables you to refine your search to match your budget. When you do find a home that you love in your price range, you have the peace of mind to proceed to auction or make an offer.

No comments:

Post a Comment